Are you a homeowner who has recently discovered a leaky or damaged roof? Roof replacement can be a costly expense that many of us are not prepared for. The unexpected nature of such repairs can often cause anxiety, leaving us uncertain and worried about how we will come up with the funds to cover the expense. While fixing your roof is essential from a safety standpoint, it is also vital to ensure that you’re not placing yourself or your family at financial risk to do so. In this blog, we will discuss various financing options available to homeowners, providing insight and guidance on financing an unexpected roof replacement while overcoming the anxiety it may bring.

Consider Using the Equity in Your Home

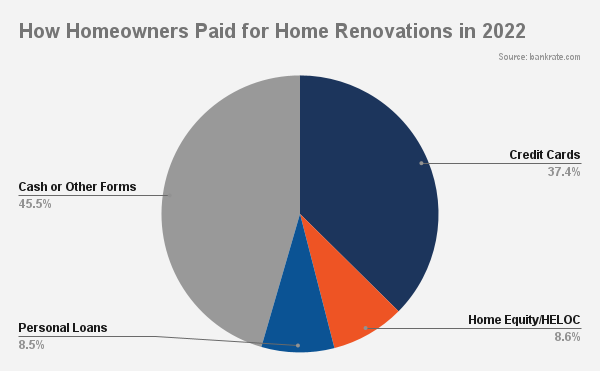

Leveraging home equity can be an effective solution when financing a roof replacement. There are two common ways to tap into home equity. The first is by utilizing a home equity loan. The second is with a home equity line of credit (HELOC).

Home Equity Loan

A home equity loan allows homeowners to borrow a lump sum against the value of their home. Typically, it is repaid over a fixed period with a fixed interest rate. When homeowners use a home equity loan to finance a roof replacement, they can use the equity they have built in their property to secure a substantial amount of funds upfront. This option provides borrowers a predictable repayment schedule and often offers lower interest rates than other financing options.

HELOC (Home Equity Line of Credit)

A home equity line of credit (HELOC) is a line of credit that homeowners can access as needed. A HELOC operates similarly to a credit card and allows borrowers to borrow funds up to a certain limit during a specific period, known as the draw period. Homeowners can use this line of credit to cover roof replacement costs as they arise. Unlike a home equity loan, interest is only paid on the amount borrowed. HELOCs offer flexibility and allow homeowners to borrow smaller amounts as needed, making them suitable for ongoing or unpredictable expenses.

A home equity line of credit (HELOC) is a line of credit that homeowners can access as needed. A HELOC operates similarly to a credit card and allows borrowers to borrow funds up to a certain limit during a specific period, known as the draw period. Homeowners can use this line of credit to cover roof replacement costs as they arise. Unlike a home equity loan, interest is only paid on the amount borrowed. HELOCs offer flexibility and allow homeowners to borrow smaller amounts as needed, making them suitable for ongoing or unpredictable expenses.

HELOCs and home equity loans can be valuable options for financing a roof replacement, depending on individual circumstances. It is crucial to carefully consider these financial products’ terms, interest rates, and repayment plans to ensure they align with your financial goals and capabilities.

What Could Go Wrong?

Financing a roof replacement using a home equity loan or a HELOC can offer advantages, but there are also potential risks to consider.

One potential risk is that both options use your home as collateral. You could lose your home if you default on the loan or fail to make the required payments. It’s important to carefully assess your ability to make the monthly payments and ensure you have a solid plan for repayment.

Another risk to be aware of is the potential for overleveraging your home. Taking out a large loan against your home’s equity could leave you with little equity remaining and reduce your financial flexibility, making it harder to sell or refinance your home in the future. Additionally, if you take out a loan and your property value declines, the HELOC may be paused since its use is determined based on how much equity is in your home.

Interest rates are another consideration. While home equity loans and HELOCs often offer competitive interest rates, they are still subject to market conditions and can fluctuate over time. It’s crucial to understand the terms of the loan, including whether the interest rate is fixed or variable, as the terms impact your monthly payments.

Interest rates are another consideration. While home equity loans and HELOCs often offer competitive interest rates, they are still subject to market conditions and can fluctuate over time. It’s crucial to understand the terms of the loan, including whether the interest rate is fixed or variable, as the terms impact your monthly payments.

Additionally, when using a HELOC, homeowners have a revolving line of credit from which they can draw as needed. This can tempt some people to use the funds for non-essential expenses, leading to increased debt and potential future financial difficulties.

To mitigate these risks, it’s essential to carefully evaluate your financial situation and consider your ability to repay the loan. Consulting with a financial advisor or mortgage specialist may be a wise thing to do to fully comprehend the potential risks and benefits of using a home equity loan or a HELOC to finance a roof replacement.

What About Credit Cards?

Credit cards can be a quick way to finance home renovation projects, including roof replacements. However, like any financing option, there are pros and cons to consider.

Pros:

- Accessibility: Credit cards are easy to obtain and provide quick access to funds.

- Flexible repayment: Credit card balances can be repaid over time, providing flexibility in managing cash flow and the ability to make smaller payments over a more extended period.

- Rewards and benefits: Many credit cards offer cashback and rewards programs or other benefits such as travel insurance or extended warranties. If used responsibly, these rewards can provide value for homeowners.

- No collateral: Unlike home equity loans or HELOCs, credit cards do not require collateral.

- Low introductory interest rates: Some credit cards offer zero percent or low interest rates for a period, allowing homeowners to spread out payments without incurring high interest charges.

Cons:

- High-interest rates: Credit card interest rates are usually higher than home equity loans or HELOCs, making them a more expensive option in the long term.

- Limited funds: Credit card limits may not be sufficient to cover more significant expenses like roof replacements. In this case, homeowners may need to apply for multiple credit cards, which can further increase the risk of high-interest debt.

- Potential for debt: Using credit cards to finance home renovations can lead to debt if the balance isn’t paid in full each month. High balances can negatively impact credit scores and make it harder to obtain financing in the future.

- Variable rates: Credit card interest rates are variable and can change over time, unlike home equity loans or HELOCs, making it harder to calculate the final cost of financing your roof.

- Impact on credit score: Using a high percentage of your credit card credit limit can lower your credit score, making it more challenging to access future financing options and leading to higher interest rates.

Overall, using a credit card to finance a roof replacement or other home renovation project may be a viable option for homeowners with good credit and the ability to pay off the balance quickly. However, credit cards often come with high-interest rates and limited funds, making it essential to carefully evaluate the terms, fees, and repayment plans before moving forward with this financing option.

Personal Loans, Including Financing Through a Roofing Company

Homeowners often use personal loans to acquire the needed funds for a home improvement project like a roof replacement. Utilizing a roof financing company to finance your project can provide several benefits: